Self-Funding & Stop-Loss: Rethinking the Risk Equation

June 23, 2025

June 23, 2025

In a benefits world where cost control is king and flexibility is increasingly prized, self-funding has stepped into the spotlight. Once viewed as something only for large corporations, this model is now gaining traction with smaller groups, especially as stop-loss coverage continues to evolve and make self-funding more accessible.

Whether you're advising an employer who's exploring self-funding for the first time or refining a strategy for a seasoned client, understanding how self-funding and stop-loss work together is essential. And beyond understanding the mechanics, it helps to know what these strategies offer, who they’re best suited for, and how they’re likely to evolve.

The Fundamentals of Self-Funding

At its most basic level, self-funding means the employer takes on the financial responsibility for health care claims instead of paying fixed premiums to a traditional insurance carrier. Rather than writing a check each month to cover projected costs and insurer profit margins, the employer pays claims as they occur.

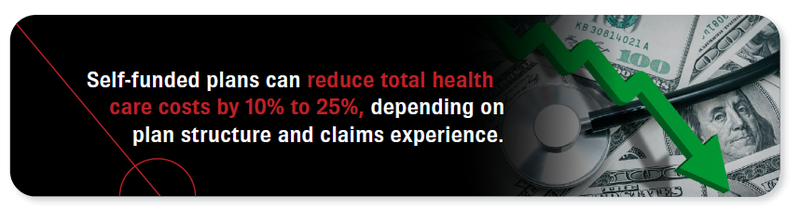

This approach gives employers more control over the structure of their benefit plans, allows greater visibility into spending, and opens the door for cost savings when claims run low. If fewer claims come in than expected, the employer can retain the unused funds. Unlike fully insured models, where the carrier sets the rates and pockets the surplus, self-funding offers a clearer link between actual health care use and overall cost. For many employers, that link translates into real savings. Estimates suggest that moving to a self-funded model can reduce total health care costs by 10% to 25%, depending on plan structure and claims experience. 1

That said, self-funding carries a degree of risk. A year with unexpectedly high claims can create financial strain. That’s why many employers partner with a third-party administrator (TPA) to manage claims processing, compliance, and reporting. They also purchase stop-loss insurance to protect against large or unpredictable claims events. This layered approach allows employers to take advantage of self-funding without exposing themselves to unlimited downside.

How Stop-Loss Coverage Helps Balance Risk

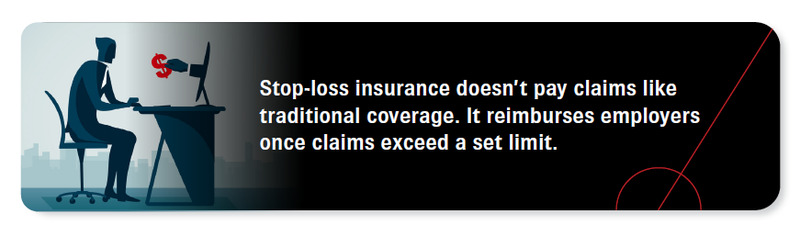

Stop-loss insurance acts as a buffer between a self-funded employer and significant claim exposure. It doesn’t pay claims directly the way a health insurance carrier would. Instead, it reimburses the employer when claims exceed a predetermined limit.

There are two main types of stop-loss coverage.

Stop-loss insurance doesn’t pay claims like traditional coverage. It reimburses employers once claims exceed a set limit.

Employers can tailor stop-loss coverage to match their tolerance for risk. Attachment points, coverage thresholds, and premium costs can all be adjusted to align with budget needs and financial goals. Some may opt for lower attachment points and higher premiums to limit exposure. Others are comfortable taking on more risk to reduce fixed costs.

The flexibility and security that stop-loss coverage offers has made self-funding a realistic option for more employers than ever before. Smaller and mid-sized businesses that once viewed self-funding as too risky are now taking a second look. Often, that decision is supported by experienced advisors and updated plan design tools.

Which Employers Should Consider It?

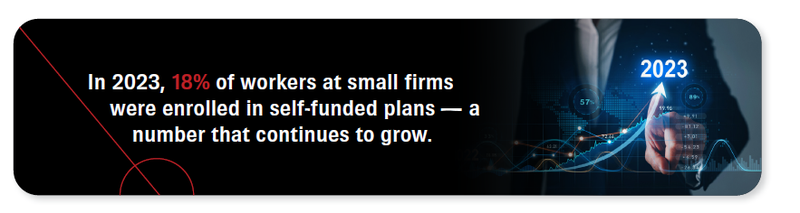

Self-funding used to be a space dominated by large employers with in-house HR teams and the financial muscle to handle risk. That landscape has changed significantly, and recent data backs that up. In 2023, 18% of covered workers at small firms were enrolled in self-funded plans, reflecting a steady increase from prior years.2

As new funding strategies and advanced analytics have emerged, self-funding is now a viable path for a broader range of employers. That includes mid-sized businesses, nonprofit organizations, and even smaller companies with a relatively healthy workforce.

Self-funding can be a strong fit for employers that:

This approach won’t work for every group. It requires a certain level of financial stability and a willingness to engage more actively in plan management. But for the right employer, it offers an opportunity to create a benefits strategy that aligns with both budget and culture.

Why Advisors Should Be Paying Attention

Employers are under pressure from rising health care costs and tighter budgets. Many are looking beyond rate relief and focusing on strategies that offer real value for their workforce and their business. This shift creates opportunities for advisors who can offer clear, actionable alternatives backed by solid planning.

Advisors who can guide clients through the full scope of self-funding, including evaluating feasibility, shaping plan design, and implementing stop-loss coverage, add measurable value. These conversations go beyond annual renewals and into long-term planning.

For some employers, the idea of self-funding may be new or feel complex. Others may have considered it before and are ready to revisit the model with a fresh perspective. In both cases, clients rely on their advisor to bring clarity, anticipate concerns, and help them make informed decisions. That level of support builds stronger partnerships and positions the advisor as a key part of the client’s strategy moving forward.

The Role of the TPA and Other Support Partners

A successful self-funded strategy depends on having the right support system in place. Most employers [RF1] are not equipped to handle claims processing, provider networks, or compliance requirements themselves. Fortunately, they don’t have to.

Third-party administrators (TPAs) handle the operational side of self-funded plans. That includes claims adjudication, customer service, reporting, and sometimes provider negotiations. Choosing the right TPA is critical. A strong TPA can enhance the employer’s experience and deliver savings through more efficient claims management. A poor fit can lead to confusion, a lack of transparency, and an increased administrative burden.

In addition to TPAs, many brokers lean on partners to help with pharmacy benefit management (PBM) strategies, population health data, or compliance guidance. These relationships can be key to building a holistic, effective benefits offering.

Looking Ahead: A Growing Space with Growing Expectations

Interest in self-funding isn’t slowing down. The self-insured market is projected to grow at approximately 2% annually through 2030, driven by continued cost pressures and the demand for greater flexibility.³ This flexibility applies not only to plan design but also to the ability to incorporate best-of-breed point solutions, rather than relying on the canned, one-size-fits-all offerings typical of fully insured plans.2 Enhanced stop-loss products, more competitive TPAs, and the integration of advanced data analytics are making self-funding not just possible but increasingly attractive. Employers want more control. They want visibility. They want options that go beyond reacting to annual rate increases. Self-funding, when structured well, delivers on all of that. While it does come with risk, those risks can be managed with the right setup, the right partners, and the right guidance.

Bottom Line

Self-funding isn’t the solution for every employer, but it’s becoming a critical part of the conversation. Many organizations are looking to take a more proactive approach to health care benefits. The combination of control, customization, and financial protection makes self-funding a compelling option for the right group.

At CRC Benefits, we work closely with top stop-loss carriers, leading TPAs, and knowledgeable advisors to build smart, sustainable self-funded strategies. Whether your client is just starting to ask questions or ready to make the shift, we can help you build the right solution from the ground up.3

Now is the time to revisit self-funding as a core part of your advisory approach. If you’re not already talking about it, your competitors probably are. If you believe that self-funding may be right for you and your clients, please reach out to your CRC Benefits Sales Executive to discuss how we can help.

Contributor: Randy Foster is a Senior Consultant for CRC Benefits’ Self-Funded Division.

End Notes