The PCORI Fee: Compliance + Purpose for 2025

June 23, 2025

June 23, 2025

Why this overlooked tax still matters and what brokers need to know to keep clients on track

PCORI is drawing more questions than usual this year. With rising costs, shifting plan designs, and another round of inflation-adjusted updates, many employers are unsure what applies to them or who is responsible for the paperwork. For brokers working with self-funded or level-funded groups, this is a timely opportunity to provide guidance and reinforce value.

This year’s updates include a new per-member fee amount, a consistent July 31 filing deadline, and important considerations for HRAs and plan combinations. As always, the details matter. Now is a great time to revisit the rules and make sure your clients are on solid footing.

What is the PCORI Fee, and Why Does It Matter?

The PCORI fee often flies under the radar, especially compared to more high-profile compliance tasks. But it plays an important role in funding research that improves how care decisions are made. The Patient-Centered Outcomes Research Institute, created by the Affordable Care Act, is not a government agency, but a nonprofit that has awarded more than $4.5 billion in grants to study real-world health outcomes.1

From maternal health to mental health, PCORI-backed research has influenced real-world issues and is driving better results for patients across the country. Employers who contribute to the fee, whether they realize it or not, are helping support that mission.

How Much Is the Fee in 2025?

Each year, the PCORI fee is adjusted for inflation, and the amount depends on when the plan year ends. For plans that end between January 1 and September 30, 2024, the fee is $3.22 per covered life. For plan years that end between October 1, 2024, and September 30, 2025, the updated amount is $3.47 per covered life.2

These numbers may seem small, but the total cost can increase quickly for larger groups. It’s important to make sure your clients are using the correct rate for their plan year.

The PCORI fee is reported once per year using IRS Form 720, filed for the second quarter and due by July 31, 2025. Employers should confirm they are using the most current version of the form by visiting the IRS website.

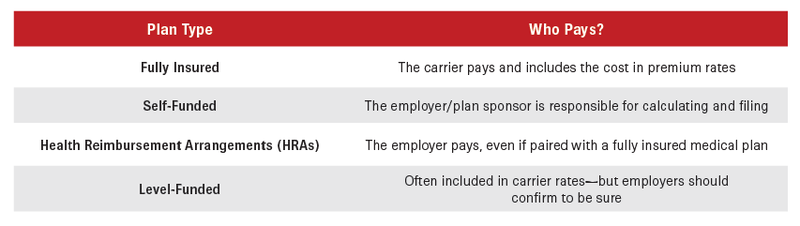

Who Needs to Pay?

Responsibility for the PCORI fee depends on the type of health plan offered.

Note: The fee does not apply to standalone dental or vision coverage, most FSAs, wellness-only programs, or government programs like Medicare or Medicaid.

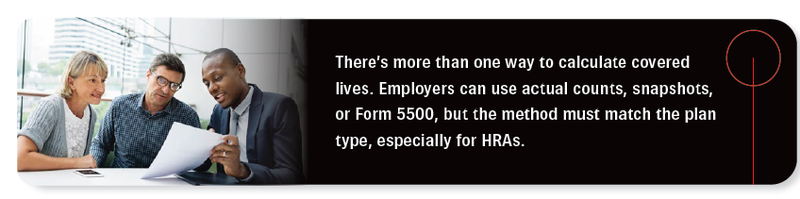

Calculating the Covered Lives

Because the PCORI fee is based on the number of covered lives, accuracy matters. Covered lives usually include both employees and their dependents. The IRS allows several methods to determine this number, giving employers flexibility based on the type of data they have.

The Actual Count Method involves counting the number of covered individuals on each day of the plan year and dividing by the total number of days. This method provides a detailed average but may require more data than some employers have available.

The Snapshot Methods are a bit simpler. With the Snapshot Actual Method, employers pick one or more dates in each quarter, count the covered lives on those dates, and calculate the average. The Snapshot Factor Method is another option for traditional group plans. Employers count all self-only participants, then add 2.35 times the number of participants with dependent coverage. However, this approach cannot be used for HRAs or FSAs.

Finally, the Form 5500 Method works for employers who file Form 5500 on time and without an extension. If the plan provides only self-only coverage, the employer adds the participant count at the beginning and end of the plan year and divides by two. If the plan includes dependent coverage, the beginning and end counts are added together without averaging.

For employers offering a Health Reimbursement Arrangement (HRA), the calculation can be simplified. In most cases, only employees need to be counted, and dependents can be excluded.

Special Considerations for HRAs and Multiple Plan Combinations

Some employers offer more than one type of health plan, and that can make PCORI fee responsibilities a little more complex. How the fee is calculated depends on how the plans are structured and whether they are insured, self-funded, or combined with an HRA.

When an HRA is offered alongside a fully insured medical plan, the IRS treats them as two separate plans. The insurance carrier handles the fee for the insured plan, and the employer is responsible for the HRA portion. In this case, the employer can count only employees when calculating the fee and does not need to include dependents.3

If an HRA is paired with a self-funded medical plan, the IRS considers them one combined plan. That means both employees and dependents must be counted, but only once.

Some employers may sponsor multiple HRAs in addition to a fully insured health plan. When that happens, the HRAs are often treated as one combined arrangement. The employer is still responsible for the HRA fee and can count just the employees. The carrier will take care of the insured portion separately.

Getting the classification right is important. Mistakes in how these plans are counted or reported can lead to overpayment, missed fees, or IRS follow-up.

Why This Matters for Brokers

PCORI often slips through the cracks, which is why it gets mishandled. Some employers don’t realize they need to file. Others miscalculate lives or use the wrong rate. HRAs can be especially confusing. Level-funded groups may assume the carrier is handling it, when that’s not guaranteed. These errors can lead to audits, penalties, and frustrated clients.

The PCORI fee may be once a year, but it’s a good checkpoint that shows whether plan setup, funding, and filing are working as they should. Clients remember who caught the issue before it became a problem, and brokers who get ahead of this are credible and indispensable.

Bottom Line

The PCORI fee may seem minor, but the impact of getting it wrong can be serious. More than just a compliance task, it helps fund research that influences how care is delivered and how coverage decisions are made. It connects compliance with meaningful outcomes.

At CRC Benefits, we give brokers the tools and support to stay one step ahead. Our compliance team helps you understand the rules, apply them correctly, and guide your clients with confidence. We simplify the process, answer tough questions, and provide the kind of partnership that builds long-term trust. When your clients rely on you for timely, accurate support, you need a team behind you that is just as committed.

If you have questions or want to walk through a specific scenario, your CRC Benefits team is ready to help. We’re here to make compliance easier and ensure your clients are always prepared.

Contributor: Misty Baker is the Director of Compliance and Government Affairs for CRC Benefits.

End Notes: