Why DEI Rollbacks Are Raising New EPL Concerns

January 29, 2026

January 29, 2026

As Diversity, Equity, and Inclusion (DEI) policies face increasing scrutiny, the risk landscape for employers is rapidly evolving. DEI programs, once viewed primarily as cultural or reputational assets, are now emerging as a focal point for legal challenges and employment practices liability (EPL) claims. Shifts in federal and state policy and heightened attention from the EEOC and investor groups are creating EPL exposure, whether an organization scales back DEI initiatives or maintains them.

Employers are finding themselves in a challenging position: reducing DEI programming can lead to claims of discrimination or retaliation, while continuing such efforts may expose them to accusations of reverse discrimination or shareholder litigation. This dual-edged risk makes it increasingly important to understand how policy decisions intersect with EPL insurance protection.

WHY IT MATTERS FOR ALL LINES OF COVERAGE

While this analysis focuses on Employment Practices Liability (EPL) exposures often seen on the Property & Casualty side, DEI policy shifts affect every employer. For health and life brokers, these same trends influence HR policy decisions, benefit design, and workplace culture; all areas directly tied to compliance, employee well-being, and plan participation.

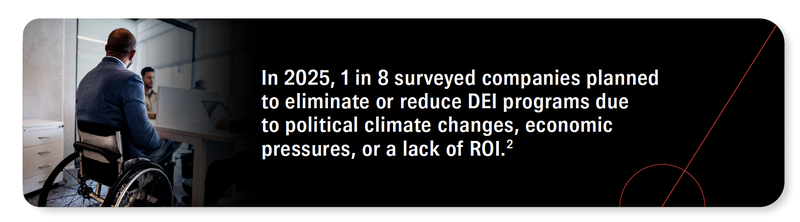

WHAT’S CHANGING IN DEI POLICY?

At the federal level, executive orders and administrative policies are rolling back previous DEI-related mandates, particularly in education and government. These efforts include restrictions on DEI training, defunding of related offices, and reversals of affirmative action precedent. Some states are following suit, passing laws or executive actions restricting race-based initiatives and requiring compliance reviews.

The Department of Justice has also introduced a task force to investigate potential civil rights violations by federal funding recipients. These developments create uncertainty for employers, who must balance their internal DEI commitments with a fast-changing legal landscape.

THE EPL IMPACT: RISKS FROM BOTH SIDES

Employers that reduce or eliminate DEI programs may face claims from employees who allege a hostile work environment or diminished support for protected groups. Retaliation claims tied to previous DEI activity are also a potential outcome. On the other hand, maintaining or expanding DEI programs could result in lawsuits from employees or applicants who perceive themselves as unfairly disadvantaged, commonly referred to as reverse discrimination claims.

Section 1981 claims under the Civil Rights Act are becoming more prevalent, especially when programs are perceived to exclude individuals based on race or other protected characteristics. The recent Students for Fair Admissions case has prompted broader scrutiny of race-based scholarships and hiring programs in the education sector. In the private sector, shareholder lawsuits are also rising, with investors alleging that companies have misrepresented or mishandled the financial impact of their DEI strategies.

This combination of pressures creates a volatile environment where legal defensibility is uncertain, especially given inconsistent guidelines across jurisdictions.

WHAT’S AT STAKE IN EPLI COVERAGE

While insurers have not yet made sweeping changes in response to these emerging DEI exposures, brokers and insureds should be vigilant. Policies should be reviewed for how they define “wrongful acts,” ensuring coverage includes a wide range of employment-related claims such as discrimination, retaliation, and negligent hiring or promotion practices.

It’s essential to verify whether the policy includes third-party coverage, protecting against claims made by job applicants, vendors, or clients, not just employees. Employers using outdated EPLI forms or relying on a general liability rider may lack this essential protection.

Brokers should also be aware of potential exclusions related to government investigations, regulatory actions, or intentional conduct. Some class-action and EEOC claims may be subject to sublimits, and EPL exclusions in D&O policies may limit protection from related shareholder lawsuits.

WHAT RETAIL BROKERS CAN DO

Retail brokers can help clients navigate this landscape by encouraging proactive internal review of DEI policies and related documentation. Employers should assess which programs are in place, how those initiatives are defined, and whether legal counsel has reviewed them in light of current anti-discrimination laws.

Training for leadership teams should emphasize the objective, legally sound implementation of company policies. Employers should document their rationale for any DEI-related changes and ensure hiring, pay, and promotion decisions are based on clear, merit-based criteria.

From an insurance perspective, now is the time to reevaluate EPLI policy language. Brokers should guide clients through key questions that highlight potential risks and gaps:

These conversations help surface hidden vulnerabilities and lead to better-tailored coverage solutions.

BOTTOM LINE

DEI policy shifts are creating new EPL exposures across the board. Whether a company is scaling back, reassessing, or doubling down on its diversity initiatives, liability is no longer a one-sided concern. Inconsistent legal frameworks, rising claims, and heightened enforcement are reshaping risk in this space.

Retail brokers have a critical role in helping clients adapt and protect themselves, and CRC Specialty offers the products, insight, and partnerships needed to make that possible. With access to leading carriers and a pulse on the latest developments, CRC is the go-to wholesale resource for EPL protection in a changing landscape. Reach out to your CRC Specialty Producer for assistance today.

WHY THIS MATTERS FOR HEALTH & LIFE BROKERS

Shifts in DEI policy are influencing far more than hiring practices. They are changing how employers approach equity, inclusion, and the overall employee experience, including benefit design and communication. As companies scale back or redefine DEI programs, the impact can reach every part of their workforce strategy, from recruiting and retention to compensation and wellness planning.

These shifts are reshaping how organizations manage both people and benefits. CRC Benefits partners can help retail brokers identify these connections and deliver a broader, people-first perspective in every client conversation.

CONTRIBUTORS

Allyson Benda has over 25 years of insurance industry experience and is an ExecPro Broker with CRC Nashville.

END NOTES